The Buckle: Steady Growth Through Conservative Management 8 comments

by: Peter Mycroft Psaras November 16, 2009 about: ANF / ARO / BKE / GPS / WMT

Peter Mycroft Psaras

The Buckle, Inc. (BKE) is a leading retailer of medium to better-priced casual apparel, footwear and accessories for fashion-conscious young men and women. The Company currently operates over 400 stores in 41 states, under the names Buckle and The Buckle.

Buckle markets a wide selection of brand names and private label casual apparel, including denims, other casual bottoms, tops, sportswear, outerwear, accessories and footwear. The Company emphasizes personalized attention to its customers and provides individual customer services such as free alterations, layaways and a frequent shopper program.

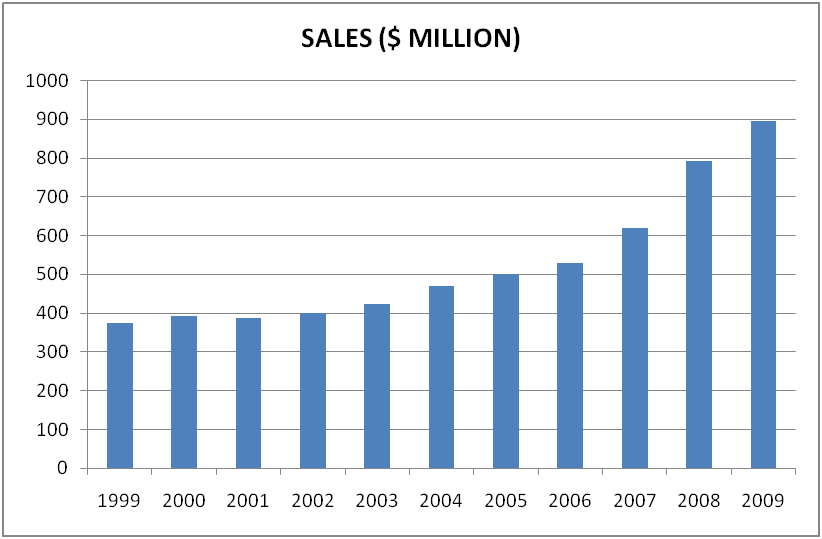

The Buckle is a very conservatively run company with excellent management at the helm and has caught my attention because of its tremendous performance on Main Street. The following charts are proof as to that performance:

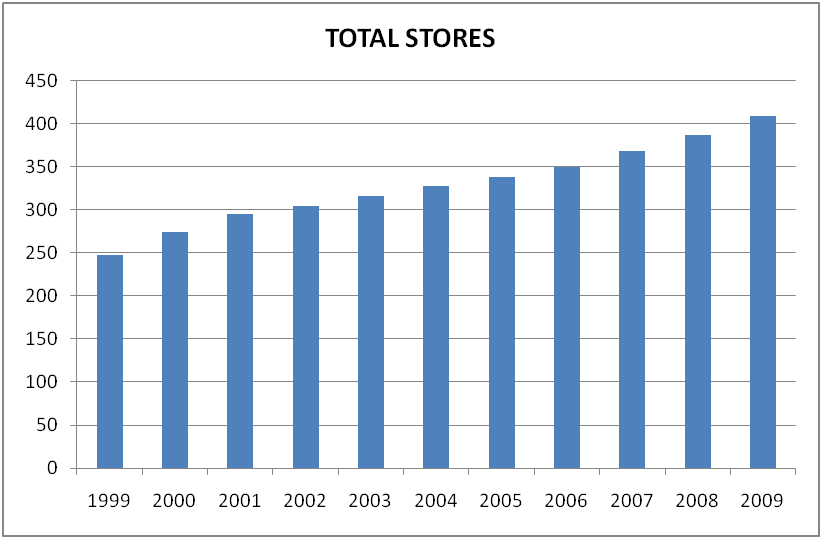

As the chart above shows, The Buckle has grown its sales 138.35% over the last ten years at an average annualized rate of 9.07%. That might not sound like much, but another company that you may have heard of, Wal-Mart (WMT), has grown its sales at about the same rate at 146% while increasing their number of stores by 115% during that time.

The Buckle on the other hand has achieved similar sales growth numbers, while only increasing their number of stores by 63.4% over the last ten years.

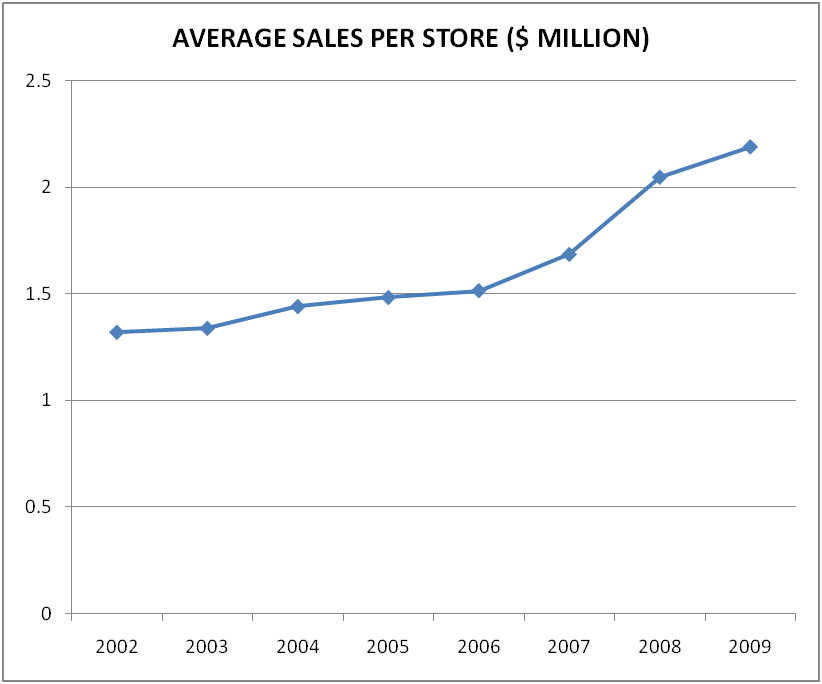

So, logically, if the number of stores has grown at a slower pace than Wal-Mart, then how it is possible to grow revenue at about the same rate? The answer is management effectiveness (a key metric of qualitative analysis and growth investing). If that is the case then how do you measure management effectiveness quantitatively? The following charts will show you.

Sales per store have gone from $1.32 million per store in 2002 to $2.19 million per store in 2009. Thus, we have a growth rate of sales per store of 65.9% over a seven year period.

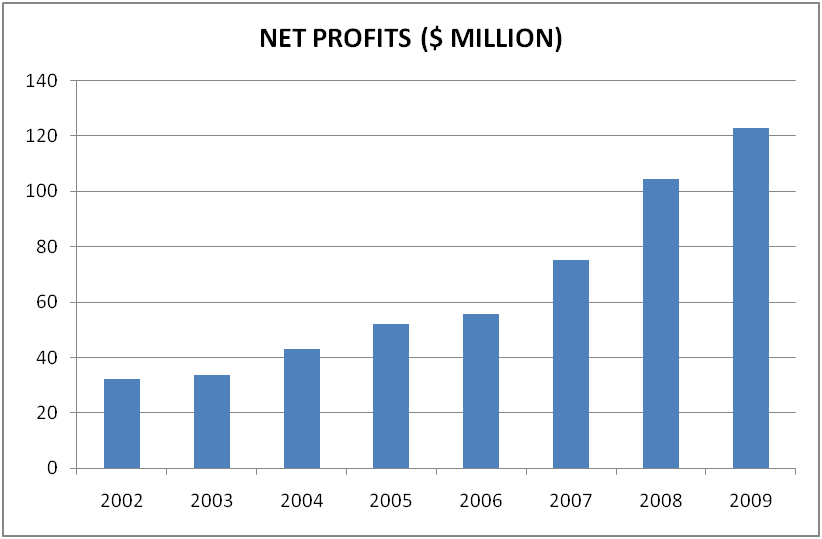

From that we can then see how the Net Profits of the company have been.

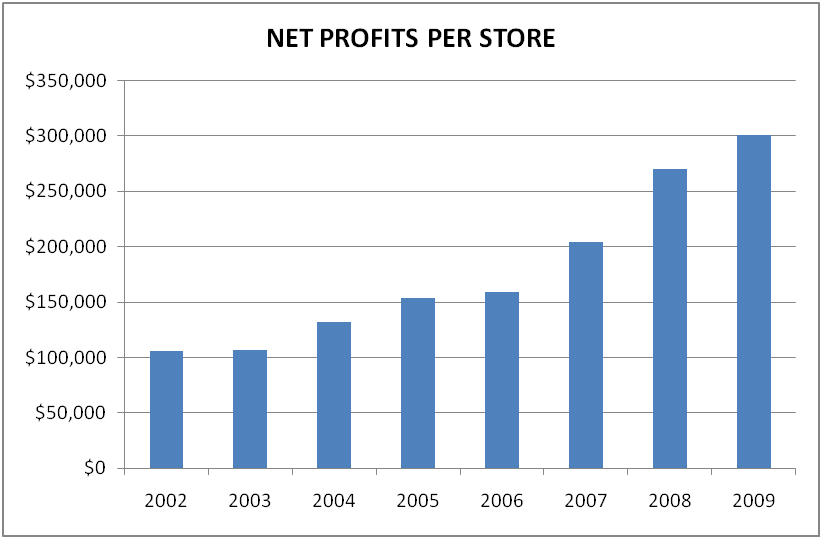

And then Net Profits per store:

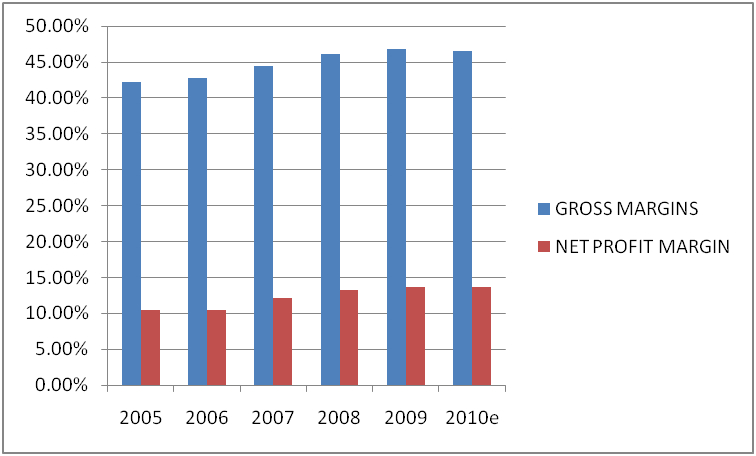

For those keeping score, that is a growth rate of 184.5% over the seven years under analysis, or an average annualized growth rate of 16.13%. When analyzing retail, one should not judge a company by its size, but should treat every company equally and see how they perform on a per store growth rate basis. The reason The Buckle has done so well is because they have grown at a conservative pace and, unlike a company like Starbucks (SBUX), for example, management did not try to put a store on every block in every corner of the world in a short period of time. That is why Starbucks stock price crashed, as it grew faster than it should have and over extended itself. The Buckle has management that is very conservative and waits for the right time to open new stores. By doing this they have been able to achieve strong margins and have consistently kept them at those levels. Here is a chart of Gross and Net Margins so you can see what I mean:

When looking for strong long term growth investments, one needs to look for consistency in order to protect oneself from surprises. For example, in 2008 Abercrombie and Fitch (ANF) had gross margins of 71%, which were much higher than The Buckle's, but net margins were only half as good. It only got worse in 2009 for ANF as net margins fell to 0.10% vs. 13.7% for The Buckle. Why was this? ANF had the same problem as Starbucks and opened too many stores too quickly and got hit hard when the recession came about. The Buckle’s management practices proper planning and prepares for the “worst case” scenario and not “best case” as many of its competitors do.

In this recession (that is now ending), you hear that no one is hiring and that things are doom and gloom. That is not the case though with The Buckle. If you go on their jobsite you will see that they have 2,776 job postings. The Gap (GPS) for example, which has 9 times as many stores as BKE has only 408 job postings. Why would The Buckle be looking to hire so much if they felt they were in trouble?

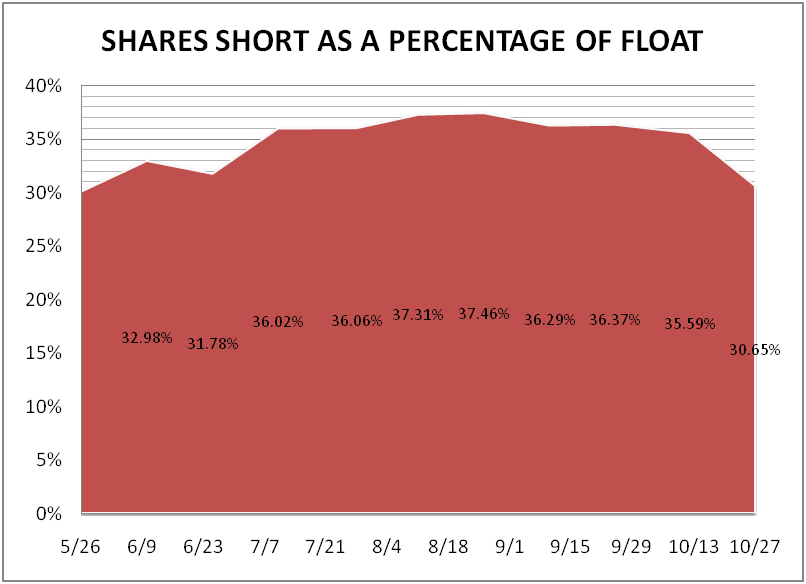

If you look at the opinions of Wall Street concerning the company you would think that the Buckle is close to bankruptcy. Schwab for example ranks the company an “F” and Goldman Sachs the other day downgraded the company to a “Sell.” The company is also one of the most heavily shorted stocks on Wall Street, coming in with a current total of 30.7% of outstanding float being short. Here are some charts:

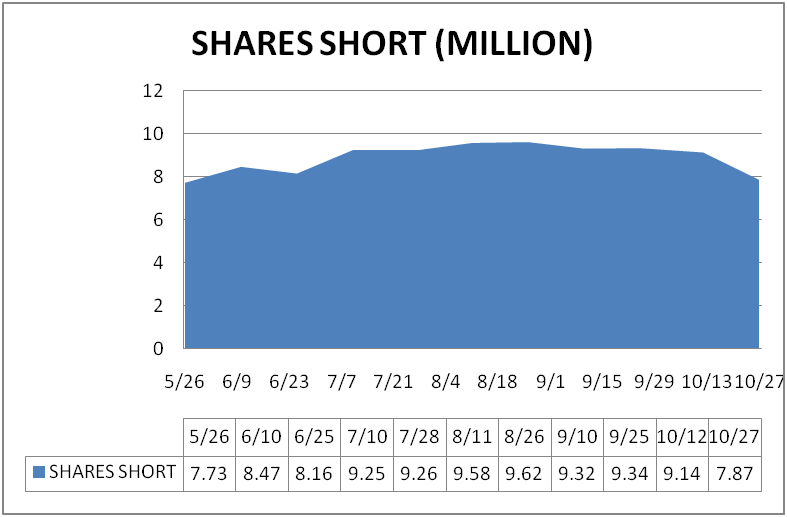

And total number of shares short:

I have analyzed this company from every angle you can imagine and for the life of me, I have not been able to find a good reason to short this stock. The only reason I can come up with is that the float outstanding is only 25.8 million shares, as management and directors own 46.1% of the shares outstanding.

With The Buckle you have a company that has $3 a share in cash, a current ratio of 3.70 and has zero total debt. Management is expanding into the northeast for the first time and is hiring 2,776 new employees to do so. If the business model has been very successful in the 41 states that it operates in, then why would it not be in the remaining northeast states? Are the teens any different in those states? I don’t think so and, in fact, their parents' per capita income is probably higher, so a mid-priced teen retailer should thrive in the northeast, especially when teens can get their purchases altered for free (The Buckle has in-store seamstresses and tailors). Where can you find that level of customer service among their competition?

Now, having so many shares short could create a nice opportunity to purchase The Buckle in the near future, especially if it were to miss its earnings estimates for the quarter when it reports on November 19, 2009. For those who own it, if they miss it might be a good chance to double down as the company, obviously, from what I have shown above, has tremendous growth prospects ahead of it.

But let us say that the company doesn't miss? What do you think will happen if it beats estimates to all those short sellers? They will have the short squeeze of the century happen as 30.7% of the float will need to be covered. And, as one short seller covers, it will put tremendous pressure on everyone else to do so or get slaughtered.

Aeropostale (ARO), which reports on December 2, 2009, can be thought of as a similar situation though it does not have Officers and Directors owning as many shares or short sellers shorting the stock so heavily.

But before investing in the company it is critical to do some backtesting on BKE. How would you have done owning the stock in the past? Especially, one that has management owning such a large chunk of the shares outstanding. Is such large ownership a benefit or a detriment to the underlying stocks performance on Wall Street?

The stock price of BKE in May of 1992 was $1.64 and was $29.14 on November 13, 2009, for a return of 1,676% over 17 years or an 18.44% average annualized gain. What the numbers above don’t show you is that, over the last three years, The Buckle has paid out a special dividend of $1.33 in 2007, $2.00 in 2008 and $1.80 in 2009. Those were on top of the 3% dividend that the company pays out on average every year. I don’t know if the special dividends will continue in the future but, if they do, it sure adds tremendous value to the long term shareholder.

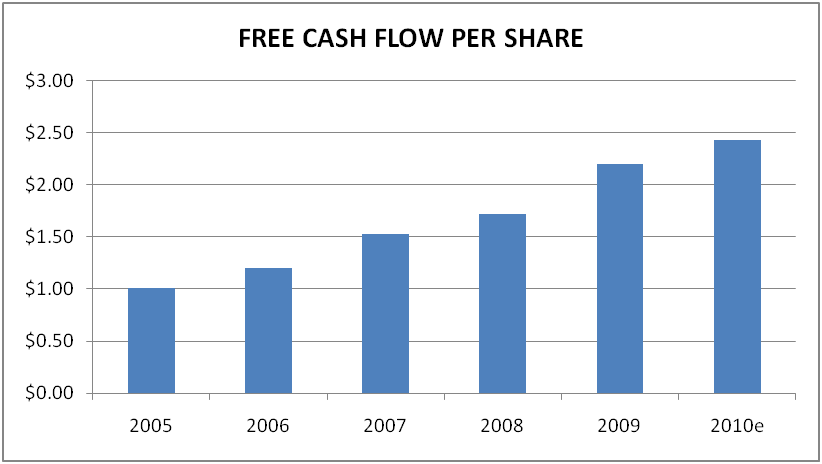

But, since the Company has no debt, how is it that it is able to pay out such amazing dividends? The answer quite simply is that it generates tremendous free cash flow as the following charts will show:

Free Cash Flow per share has been wonderful at the company and has gone from $1.01 in 2005 to an expected 2010 estimate of $2.43, which amounts to a growth rate of 140.59% in 5 years or an annualized average return of 19.19%.

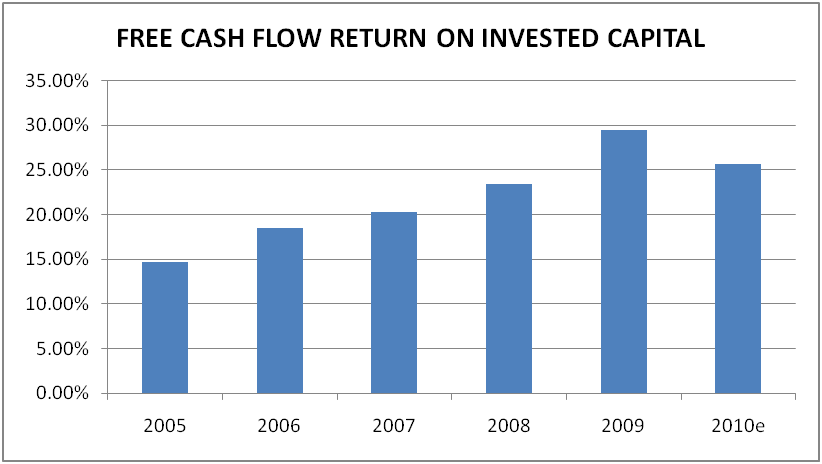

If we go one step further, we can analyze the company by its (FROIC) Free Cash Flow Return on Invested Capital. FROIC basically tells you how much return in free cash flow a company generates for every dollar of Total Capital they employ.

I consider FROIC the primary determining factor in identifying growth companies as you can compare every company (except financials) on an equal basis. The question I ask about every company I analyze is: 'how much return (in percent) in FCF are you going to give me for every dollar of total capital you invest?'

Let’s see how The Buckle has done of the FROIC scale:

So for every dollar of capital employed BKE has returned 25-30 cents of free cash flow to the company. FROIC gives me a real return on Main Street and if I can get a 20%+ return on Main Street and at the same time buy a stock that is selling for less than 15 times its FCF then there is a very high probability that it should be a very successful investment.

How is The Buckle doing on its Price to Free Cash Flow?

2010 estimated Price to Free Cash Flow (PFCF) = 10.23

As for PFCF, I came up with the 15 or less number as being Ideal after performing a 58 year backtest. Click here to view the backtest.

In conclusion, I have no idea how the company will report on November 19th, but with all the negativity that surrounds the stock, a contrarian bull case could certainly be made.

Disclosure: Long BKE , ARO, No position in ANF,WMT,SBUX,GPS

SeekingAlpha.Initializer.LogAndRun(load_article_toolbar);

Related Articles

http://seekingalpha.com/article/173657-the-buckle-steady-growth-through-conservative-management

The charts for these figures can be viewed on the above sight to get a better idea of what the numbers are looking like. Like this article says, Buckle is a great place to buy casual apparel and a median price. They have everything you could possibly be looking for, at good quality for fair prices and with great services. Lets keep it up and help this company continue to grow.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

No comments:

Post a Comment